Confused between an overdraft facility and a personal loan? Examine OD limit interest rates and personal loan options for you, and find the best borrowing option for your needs. Whenever you need quick funds, whether it is for a medical emergency or a business expense, two options often come to mind: an overdraft facility and a personal loan. Both are popular credit products offered by banks and financial institutions in India, but they work very differently.

If you are considering a 25 lakh loan for personal needs or even a 5 lakh business loan to manage operations, choosing the right product can save you thousands in interest. This article breaks down the key differences, compares the OD loan interest rate with personal loan rates, and helps you decide which option suits your financial situation best.

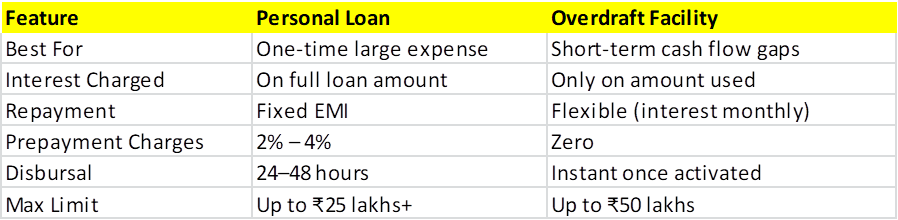

What Is an Overdraft Facility?

An overdraft facility is a flexible credit arrangement where your bank allows you to withdraw more money than what is available in your account. Where you only pay interest on the amount you actually use, not on the entire sanctioned limit.

For example, if your OD limit is ₹10 lakhs and you use only ₹3 lakhs, the OD limit interest rate applies only to that ₹3 lakhs. This makes it a highly flexible, efficient, and cost-efficient borrowing tool, especially for short-term needs.

Get a pre-approved OD limit of up to ₹50 lakhs from the best banks and NBFCs in Mumbai with Bikesh Finserv, with approval in as little as 48 hours and interest starting from as low as 12% per annum. Interest is charged only on the amount you use and only for the number of days you use it, making it one of the most cost-effective short-term borrowing options available.

Key features of an overdraft facility:

- Interest charge only on the utilized amount

- Continual credit, repayment, and borrow again

- No fixed EMI structure

- Suitable for salaried individuals and business owners

The OD loan interest rate in India typically ranges between 13% to 18% per annum, depending on the bank, your credit score, and your income and account history.

OD Loan Interest Rate vs Personal Loan Interest Rate

This is the most critical comparison for any borrower.

If you are looking for a 25 lakh loan and are fully confident that you will repay it quickly, you can go with an overdraft facility; it can be cheaper for you because the OD limit interest rate applies only to what you use. However, for a fixed large amount requirement like a 25 lakh personal loan, a personal loan gives you certainty with fixed EMIs.

Difference Between Overdraft and Personal Loan

While both products provide access to credit, here are the differences that every borrower should understand:

1. Interest Calculation: One of the core differences between the OD loan interest rate and the personal loan interest rate is that, in an overdraft, the OD loan interest rate is charged daily on the outstanding balance. While in a personal loan, interest is calculated on the entire principal from the start.

2. Repayment Flexibility: With an overdraft, you have the complete flexibility to repay your loan whenever you have funds available without any penalty. A personal loan has a fixed repayment schedule, and missing an EMI can hamper your CIBIL score.

3. Purpose and Loan Amount: A personal loan can be ideal for your larger, one-time requirement funds, such as a 25 lakh personal loan for home renovation or a 5 lakh business loan for working requirement capital. But when we talk about an overdraft facility, it works better for recurring short-term cash gaps.

4. Eligibility and Documentation Personal loans are generally available with minimal documentation. But in case of overdraft facilities, especially higher OD limits, they may require proof of your income and your credibility, and the most important thing is that you should be a reputed customer of that bank.

Overdraft Facility for Salaried Individuals

Many banks in India offer a personal overdraft facility for salaried individuals based on their monthly salary. Usually, the OD limit is set at 3x to 4x your monthly salary, making it a reliable option for you to manage your end-of-month cash deficits. If you are a salaried professional looking for a short-term borrowing option without the commitment of a full personal loan, this can be an excellent tool for you. The OD limit interest rate for salaried individuals is usually lower than unsecured personal loan rates, which makes it a cost-effective choice.

When to Choose an Overdraft Facility

Choose Overdraft when:

- You face short-term cash shortages of 5–10 days

- You want EMI bounce protection

- You need flexible borrowing and repayment with zero prepayment charges

Avoid overdraft when:

- You need funds for long-term usage (1–3 years)

- You prefer lower interest with a fixed EMI; a personal loan is better in that case

When to Choose a Personal Loan

You should go for a personal loan when:

- You need a large lump sum amount, such as a 25 lakh loan for a specific purpose

- When you are good with fixed EMIs for better monthly budgeting

- When you need for a longer repayment tenure of up to 5 years

- You need funds for debt consolidation, medical emergencies, or home renovation

- You don’t need to pledge any assets as collateral for an overdraft.

Does Overdraft Affect Your Credit Score?

Yes, both the overdraft facilities and personal loans can impact your credit score (CIBIL score). But while remaining within your OD limit and repaying on time, you can actually improve your creditworthiness. But if you continue to max out your OD limit or miss personal loan EMIs, it will have a negative impact on your score and make it difficult for you to get loans in the future.

Final Statement

Both an overdraft facility and a personal loan are powerful financial tools; the right choice depends entirely on your need, repayment capacity, and borrowing duration. If freedom of choice is your priority and you need short-term funds, the OD loan interest rate advantage makes overdraft a smart pick. But if you are planning for a 25 lakh loan or a structured 5 lakh business loan, a personal loan with fixed EMIs offers better financial predictability.

Hidden Costs & Risks of Overdraft

Before choosing an overdraft, be aware of these important points:

- Annual Renewal Fee: OD facilities may charge ₹1,000–₹2,000 yearly to keep the limit active

- Higher Interest Rates: OD rates are typically 2%–4% higher than personal loans

- Compound Interest Risk: Unpaid monthly interest gets added to the principal, increasing your borrowing cost

- Recall Risk: Banks can withdraw or reduce your OD limit if salary credits stop or your credit score drops

FAQs

Q. Which is cheaper, an overdraft or a personal loan?

An overdraft can be cheaper if you repay quickly, since the OD loan interest rate applies only to the amount used. For long-term borrowing, a personal loan with a fixed rate may work out more economical.

Q. Can I get a 25 lakh personal loan without collateral?

Yes. Personal loans are unsecured, meaning no collateral is required. Eligibility depends on your income, credit score, and repayment history.

Q. What is a good OD limit interest rate?

A competitive OD limit interest rate in India ranges between 13% to 17% p.a. for secured overdrafts and up to 19% for unsecured ones.

Q. Is an overdraft better for a 5 lakh business loan need?

Yes, for short-term working capital requirements. But if you need the full ₹5 lakhs for a fixed business purpose with a structured repayment plan, a business or personal loan is more appropriate.

Common Myths & Facts About Overdraft and Personal Loan

Many borrowers make wrong financial decisions because of misconceptions about these two tools. But you don’t need to worry because we are there for you to clear all your doubts.

Myth 1: An Overdraft Is Not a Loan

Fact: An overdraft is definitely a type of credit. When you use your OD limit, you are essentially borrowing money from the bank. The OD loan interest rate applies to every rupee you utilize, just like any other loan.

Myth 2: A Personal Loan Always Has High Interest

Fact: No. If you have a strong CIBIL score (750+) and a stable income, you can secure a personal loan at very competitive interest rates starting as low as 13.5% per annum from many NBFCs and banks in India.

Myth 3: Overdraft Has No Impact on Your Credit Score

Fact: Your overdraft usage is reported to credit bureaus just like a personal loan. Regularly maxing out your OD limit or failing to repay on time will adversely affect your creditworthiness.

Myth 4: Personal Loans Take Too Long to Get Approved

Fact: Digital NBFCs and banks can approve and disburse an instant personal loan within 24 to 48 hours today. With the right documentation, even a 25 lakh loan can be processed quickly.

At Bikesh Finserv, we offer both overdraft facilities and personal loans tailored to your financial needs. With OD limits up to ₹50 lakhs, approval in 48 hours, and interest starting from 12% per annum, we make borrowing simple, fast, and transparent. We offer competitive personal loan options tailored to your needs. We are here to assist you from initial to final. Let our expert team evaluate your profile and connect you with the right lender.